Part 1: How a global currency could work - a practical perspective

- TM

- Jan 6, 2020

- 3 min read

The United Nations currently recognizes 180 currencies around the world, used in almost 200 countries. Can there be one currency to rule them all? Or at least, to sit on top of them all? And should there be?

Like those who dreamed of using gold as a global currency while speaking Esperanto, fintech hopefuls are realizing that “internationalization” of sovereign - and to an extent cultural - territory is complicated. Regulation, politics, and monetary policy implications are just a few of the obstacles. And not only is it a matter of how the currency will be created and used, but also who is creating and managing the currency and its market platform (do you trust Facebook?). Ultimately, regulators will have the final say, not least due to domestic and financial stability considerations.

That said - if you can’t beat ‘em, join ‘em. Create your own currency as a sort of Frankenstein of international currencies. This is the needle which the Libra Association’s Libra currency will attempt to thread. And it really is the only way to get a global currency off the ground today.

From a practical perspective, how would this work? This will be my attempt to demonstrate using a fictitious company called Harvard Analytica Limited (HAL), who will be opening the pod bay doors to issue a global digital currency called GOLD2 (to draw an obvious parallel to a certain precious metal).

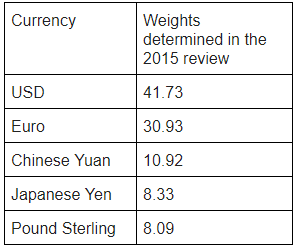

Assume that HAL wants to issue their global currency based on a basket of currencies that aligns with the IMF’s Special Drawing Rights (SDR) basket. The SDR is, in fact, an international reserve asset that is a basket of currencies, and is the unit of account of the IMF. You and I cannot buy or sell SDR, but IMF members can exchange SDR for any of currencies in the basket (read: USD).

Here is what the basket looks like as of January 2020 (note that the basket is reviewed every five years or earlier to ensure that the SDR reflects the relative importance of currencies in the world’s trading and financial systems).

These weightings will serve as the ‘guts’ of the GOLD2 global currency in this example.

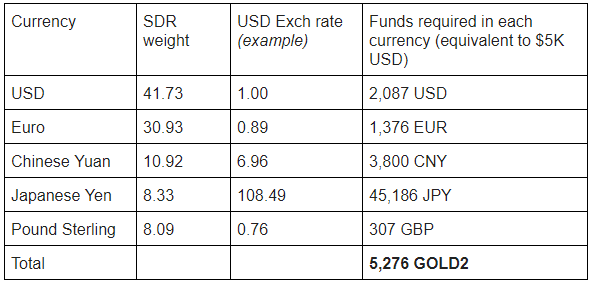

So now that the breakdown for GOLD2 is determined, HAL needs to hold this underlying basket of currencies in order to derive the GOLD2 currency. To do so, they need to have a bank, or be a bank, in each of these jurisdictions. Let’s say HAL starts with $5,000 USD seed money for which they will create their GOLD2 starting ‘float’. They will need to build the basket through the foreign exchange market by selling a certain amount of this USD seed money and purchasing the other currencies in the basket.

Note that the GOLD2 amount was determined arbitrarily by adding up the nominal amounts of each currency and dividing by 10.

We now have required amounts for each currency for a derived GOLD2 holding of 5,276 units. This also gives us an exchange rate for GOLD2/USD of 0.948.

Using this logic, we can assume that anyone who wants to hold GOLD2 can send a pay-in of any single currency which could then be exchanged by HAL to derive a GOLD2 amount for the customer - provided HAL can exchange the given currency into the five basket currencies, i.e. is ‘banked’ in the given jurisdiction. For example, $1,000 CAD could be paid in to HAL, who would exchange all the CAD for the basket currencies, to derive a GOLD2 amount.

Ultimately, there could exist published exchange rates for GOLD2 and many currencies - not just those currencies that make up the basket.

In the next part of this blog series, I will attempt to look at what transactions could look like from an account perspective, and to see how the problem of exchange rate volatility could be addressed (given that most currency holders will not want to see currency amounts in their account fluctuating - particularly on the downside, where it could resemble an unpredictable negative rate environment).

Comments